Selling a home in the Golden State usually comes with a substantial financial return, but many homeowners worry about the subsequent tax implications. Fortunately, the capital gains exclusion when selling your primary residence in California provides a significant benefit. According to the IRS’s own guidelines, most people will not owe federal or state capital gains taxes on a typical sale.

Think of this specific rule—officially known as the Section 121 Exclusion—as a tax-free boundary protecting your home equity. For single filers, this rule protects the first $250,000 of profit from the capital gains tax. Married couples filing jointly receive an even larger benefit, securing a $500,000 exclusion to safeguard their equity.

While California has high state income tax rates, the capital gains exclusion actually mirrors the exact same rules as the federal government. Because the state aligns with this federal tax break, your typical real estate profits are completely protected, letting you complete your sale with peace of mind.

Does Your Profit Fit Under the Threshold? Meeting the $250,000 and $500,000 Limits

The size of your tax exclusion depends directly on your tax filing status. If you are single or file as a head of household, the government lets you shelter up to $250,000 of profit from the sale. Couples filing jointly double that protection. Under the married filing jointly exemption, partners can protect half a million dollars of real estate profit from taxation.

If your California home appreciated significantly and your equity surpasses those limits, only the profit that exceeds your specific threshold gets taxed. For example, if a married couple buys a house for $500,000 and later sells it for $1.2 million, their total profit is $700,000. They subtract their $500,000 exclusion, leaving only $200,000 subject to capital gains. These limits represent the maximum profit allowed before paying state taxes and federal fees on the remaining balance.

Furthermore, this tax break is not a once-in-a-lifetime deal. You can apply this exclusion to a new home every two years, provided you satisfy the specific IRS Section 121 ownership and use requirements. Proving you lived in the house long enough to claim this benefit requires mastering a simple timeline.

The 2-Out-Of-5-Year Rule: Why Your Calendar is a Tax-Saving Tool

Securing these California real estate tax exemptions requires proving the property was your primary home, not just an investment. The IRS uses the two-out-of-five-years residency rule, splitting eligibility into two distinct hurdles: the ownership test and the use test. You must own the house for at least two years, and you must use it as your primary residence for 730 days out of the five years immediately before selling.

This calendar test is forgiving because those 730 days do not have to be consecutive. If you lived there for twelve months, moved away for a job, and later returned for another year, you seamlessly meet the primary residence criteria. To verify your timeline, the government looks for a practical paper trail proving:

- Where you actually slept most nights

- The address actively listed on your voter registration

- Where your regular utility bills were sent

Once you check those residency boxes, your exclusion is locked in. However, maximizing this benefit requires calculating your true adjusted cost basis to ensure you aren’t overstating your taxable profit.

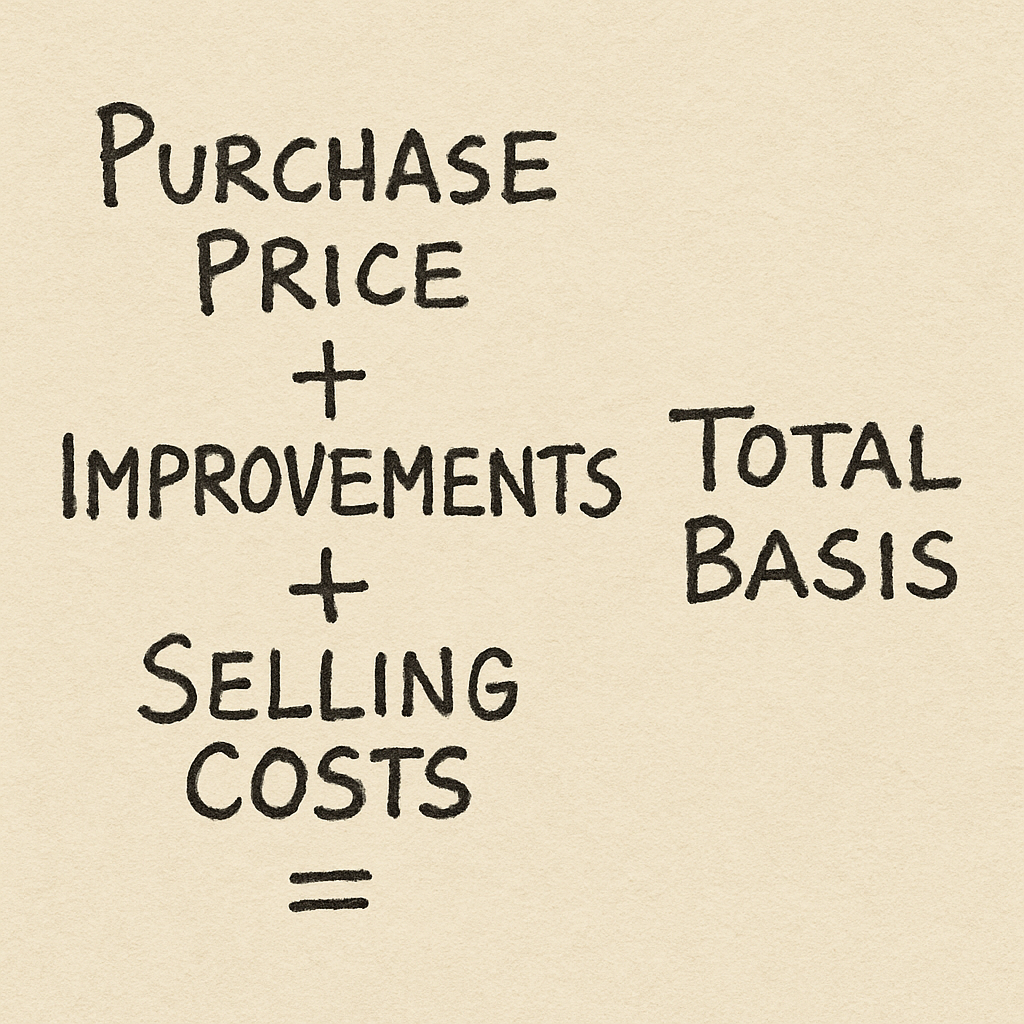

Stop Leaving Money on the Table: Calculating Your True Adjusted Cost Basis

Many homeowners mistakenly believe profit is simply the final sale price minus their original purchase price. However, the IRS allows you to adopt a “Total Spend” mindset to significantly shrink your taxable gain. This customized figure is your adjusted basis—your total financial investment in the property.

Your basis automatically increases through standard transaction fees. Deductible selling expenses for California homeowners—such as agent commissions, title insurance, and escrow fees—are added directly to your original purchase price. If you bought an $800,000 home and paid $60,000 in closing costs to sell it, your baseline instantly jumps to $860,000 before counting a single renovation.

Protecting your remaining equity also involves tracking capital improvements, though you must distinguish between permanent upgrades and routine maintenance:

- Improvement (Count it): Installing a brand-new roof, executing a full kitchen remodel, or adding central air conditioning.

- Repair (Skip it): Patching a minor roof leak, fixing a squeaky cabinet, or routinely servicing an AC unit.

Tallying every legitimate expense creates a higher baseline that lowers your taxable profit.

The California Twist: Handling Withholding and High-Income Tax Rates

Understanding your final return requires noting the crucial difference between federal and California capital gains rates. The IRS rewards homeowners with special, lower tax brackets for long-term real estate profits that exceed the exclusion limit. California, however, offers no discounted bracket. Any taxable profit left over after applying your exclusion gets taxed alongside your regular paycheck at your ordinary state income tax rate.

Escrow brings another variable: a mandatory state withholding rule that frequently catches sellers off guard. By default, California holds back 3.33% of your total sale price to cover potential capital gains taxes. You can protect your cash by carefully following the California Franchise Tax Board (FTB) Form 593 instructions. Submitting this completed form to your escrow officer certifies that your profit is fully covered by the primary residence exclusion, legally exempting you from the withholding.

Because California honors the federal $250,000 and $500,000 exclusion limits, typical homeowners rarely pay these ordinary income rates or suffer the withholding penalty, provided they meet the two-year residency requirement.

Life Happens: Securing a Partial Exclusion for Job Changes or Divorce

Unexpected life events sometimes require a move before the two-year residency clock runs out. If a sudden change forces you to sell early, you do not automatically lose your entire tax benefit. The IRS offers a partial exclusion for unforeseen circumstances, granting a prorated portion of your $250,000 or $500,000 limit based on the exact number of months you occupied the home.

To claim this benefit, the move must be triggered by unavoidable events rather than a simple desire to relocate. The IRS generally approves the following qualifying events for a partial exclusion:

- Job Relocation: Your new workplace must be at least 50 miles farther from your old home than your previous commute.

- Health Issues: Moving to obtain specific medical care or manage a severe illness.

- Divorce: Ex-spouses are often allowed to split the prorated exclusion when selling a primary residence after a separation.

- Death: Surviving spouses managing the sale of an inherited California property can use the full $500,000 exclusion if they sell within two years of their partner’s passing.

Calculating your exact tax break requires simple fraction math. If you lived in the house for 12 months—exactly half of the required 24 months—you keep half of your standard limit.

Success in the Paperwork: Exactly What to File with the IRS and FTB

Closing escrow is the final physical step, but proper documentation is required to clear the transaction with tax agencies. If your profit is fully covered by your exclusion and your escrow company does not issue a Form 1099-S, you generally do not have to report the sale. However, if you receive a 1099-S showing your gross proceeds, the IRS expects to see it detailed on your tax return.

When filing is required, bringing the correct documents to your tax preparer ensures the “Adjusted Basis” you calculated successfully protects your equity. For proper California capital gains tax reporting, you will need:

- Form 8949: To detail the home sale transaction and claim your tax exclusion.

- IRS Schedule D: To summarize your total capital gains for the federal government.

- CA Form 540: To officially apply your tax exclusion at the state level.

Cross-referencing your documents with IRS Publication 523—the official government homeowner guidebook—helps guarantee accuracy and compliance.

Your Post-Sale Checklist for a Tax-Efficient Payday

Securing the capital gains exclusion when selling your primary residence in California is an actionable, straightforward process. You can optimize your home sale tax planning by following a simple three-step strategy:

- Verify your timeline to confirm your two-year residency status.

- Create a dedicated property folder to store every remodel receipt, contractor invoice, and closing document to maximize your calculated investment basis.

- Share your adjusted basis math and completed Form 593 with your escrow officer and accountant immediately.

By organizing your documentation early, you protect your hard-earned equity. The $250,000 or $500,000 exclusion exists specifically to support homeowners building long-term wealth. With the proper paperwork and strategic planning, you can confidently finalize your sale and transition your equity into your next financial goal.